IR35 is one of the most important tax compliance issues for UK contractors, consultants, agencies, and hiring businesses. At its core, IR35 looks at whether a contractor is genuinely working as an independent business or whether the relationship looks more like employment for tax purposes.

This is why contractor agreements matter so much. A contract is often the first place clients, contractors, advisers, or HMRC look when reviewing employment status. It explains how the relationship is meant to work, who controls the services, whether substitution is allowed, how payment is made, and whether the contractor is taking real business risk.

Understanding the IR35 meaning and the main IR35 rules helps both contractors and clients reduce compliance risks. But a contract alone is not enough. The written agreement must match the real working relationship in practice.

IR35, also known as the off-payroll working rules, is UK tax legislation designed to identify contractors who work through an intermediary, such as a limited company, but operate in a way that is similar to an employee. HMRC explains that the rules are intended to make sure workers who would be employees if engaged directly pay broadly the same Income Tax and National Insurance contributions as employees.

The IR35 meaning is simple: it tests whether a contractor is genuinely self-employed for tax purposes or whether the engagement is closer to employment.

IR35 can apply where a worker provides services through an intermediary, commonly a personal service company. The rules are relevant to contractors, end clients, agencies, and fee-payers. In many public sector and medium or large-sized private sector engagements, the client is responsible for deciding the contractor’s employment status for tax and issuing a status determination statement.

The purpose of the legislation is to prevent “disguised employment.” This means a person works like an employee but uses a company structure to receive different tax treatment.

HMRC usually looks at the full relationship, including the contract, the actual working practices, and key employment status factors such as personal service, substitution, control, mutuality of obligation, and financial risk. HMRC’s CEST tool can also be used to check employment status for tax and whether the off-payroll working rules apply to an engagement.

A contractor agreement is important because it sets the legal framework for the engagement. It should show that the contractor is providing services as an independent business, not working as a disguised employee.

However, written terms are only one part of the picture. HMRC and advisers will also look at actual working practices. For example, a contract may say the contractor can send a substitute, but if the client would never allow anyone else to do the work, that clause may not help in a real IR35 assessment.

Contracts are often the first document reviewed during an IR35 assessment because they show the intended relationship between the parties. A well-drafted agreement can support an outside IR35 position, but only where the day-to-day work follows the same terms.

Poorly written agreements can create risk. A contract that refers to salary, line management, fixed working hours, employee benefits, or ongoing guaranteed work may suggest an employment-style relationship. This can increase the chance of an inside IR35 decision under the IR35 rules.

The safest approach is to make sure the contract and the real working arrangement match from the beginning.

A genuine right of substitution is one of the most important clauses in an IR35 contractor agreement. It means the contractor has the right to send another suitably qualified person to complete the work instead of doing it personally.

The clause should not exist only on paper. It should be practical and capable of being used. The client may still require reasonable checks, such as skills, security, qualifications, or insurance. But the client should not have an unlimited right to reject the substitute for no commercial reason.

This matters under IR35 rules because personal service is a key employment status factor. If the contractor must personally do all the work, the relationship may look more like employment. A real substitution clause supports the view that the client has engaged a business to deliver a service, not an individual employee.

The control clause should explain that the contractor controls how the services are delivered. This includes methods of work, technical approach, and how deliverables are completed.

The client can set project requirements, deadlines, quality standards, and commercial outcomes. But the client should not supervise the contractor like an employee or control every step of the work.

The agreement should avoid wording that gives the client control over fixed working hours, daily tasks, or employee-style reporting. It should focus on deliverables, milestones, and agreed outcomes. Location should also be flexible where possible, unless there is a clear business reason for the contractor to work on site.

Mutuality of obligation is another key factor in an IR35 assessment. The contract should make clear that the client is not required to offer continuous work, and the contractor is not required to accept future projects.

Each project should stand on its own. When the services agreement is completed, the engagement should end unless both parties agree to a new project or extension.

This helps show that the contractor is operating independently and is not part of the client’s permanent workforce.

A strong contractor agreement should show that the contractor takes some real business risk.

This may include holding professional indemnity insurance, correcting defective work at their own cost, paying for their own tools or equipment, or being responsible for business expenses. The contractor should not be protected from every risk in the same way an employee would be.

Financial risk supports an independent business relationship. It shows the contractor is responsible for delivering a commercial service, not simply being paid for time worked.

The agreement should confirm that the contractor is free to provide services to other clients, as long as there is no conflict of interest or breach of confidentiality.

This clause helps demonstrate business independence. A genuine contractor should not be tied to one client in the same way an employee usually is.

Working for multiple clients, marketing services, maintaining a business website, and having separate business records can all support an outside IR35 position.

Payment terms should avoid salary-like wording. Instead of referring to wages, salary, overtime, or employee-style pay, the agreement should use commercial terms such as project fees, day rates, fixed fees, invoices, milestones, or deliverable-based payments.

Where possible, fixed project pricing or milestone payments can help show a business-to-business relationship. Even where a day rate is used, the contract should make clear that payment is linked to services provided under the agreement.

The contractor should invoice the client or agency, and payment should be made according to agreed commercial terms.

Termination clauses should reflect an independent contractor relationship. The agreement may include a commercial notice period, immediate termination for breach, and clear end dates for project-based work.

The wording should avoid employee-style disciplinary processes, probation periods, or HR policies. The contract should show that either party can end the commercial relationship according to agreed terms.

A clear termination clause supports the idea that the contractor is an external service provider, not a permanent member of staff.

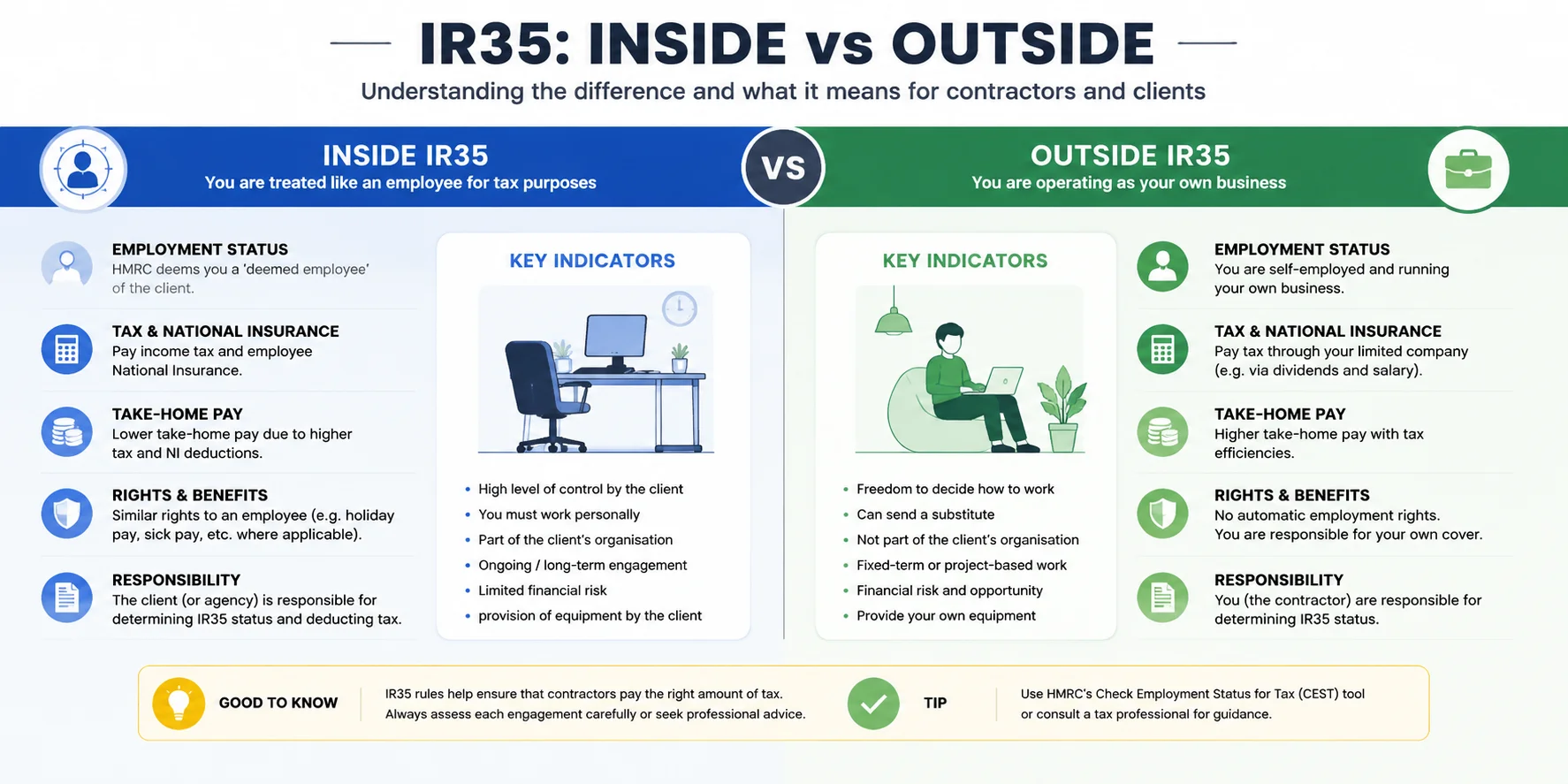

Inside IR35 means the contractor is treated as an employee for tax purposes for that engagement. In simple terms, the working relationship looks employment-like, even if the contractor works through a limited company.

People often search for the inside IR35 meaning because the tax impact can be significant. If a contract is inside IR35, Income Tax and National Insurance are usually deducted before payment reaches the contractor. Depending on the engagement, the client, agency, or fee-payer may be responsible for operating PAYE.

An IR35 inside contract may include features such as:

One important point is that inside IR35 does not automatically give the contractor full employment rights. A contractor may be taxed like an employee for that engagement but may not receive the same benefits as a permanent employee, such as holiday pay, sick pay, pension rights, redundancy rights, or unfair dismissal protection.

Outside IR35 means the contractor is genuinely operating as an independent business for tax purposes. The engagement is closer to a business-to-business relationship than an employment relationship.

The outside IR35 meaning is based on independence. The contractor controls how the service is delivered, may use a substitute, takes financial risk, and is not treated like part of the client’s workforce.

A contractor working outside IR35 usually invoices for services through their limited company and manages business taxes through that company. This can be more tax efficient, but only where the contract and working practices genuinely support self-employed status.

Examples of outside IR35 arrangements may include:

To support an outside IR35 position, the agreement should be specific, commercial, and consistent with the real working relationship.

Some contract mistakes can increase the chance of an IR35 assessment or lead to a higher-risk status outcome.

Common issues include employee-like benefits, such as holiday pay, sick pay, bonuses, staff training, or pension-style wording. These benefits can make the contractor look more like a permanent employee.

Another major issue is excessive client control. According to IR35 regulations, the relationship may be closer to employment if the client determines the contractor’s working hours, location, methods, and daily tasks.

A missing or unrealistic substitution clause is also a common problem. If the contractor has no real ability to send someone else, personal service becomes a stronger factor.

Guaranteed ongoing work can also create risk. A contract that suggests the client must keep offering work, and the contractor must keep accepting it, may show mutuality of obligation.

Other mistakes include fixed working hours, line manager approval for routine tasks, using generic contract templates, or treating contractors like permanent staff in company systems, meetings, policies, and appraisals.

The best way to prepare for an IR35 assessment is to review both the contract and the actual working practices.

Start by checking the agreement before the engagement begins. Make sure it includes the key clauses around substitution, control, mutuality of obligation, financial risk, payment terms, and termination.

Next, keep evidence of how the work is actually performed. This may include project briefs, milestone records, invoices, emails showing independent decision-making, evidence of multiple clients, business insurance, and proof that the contractor uses their own equipment where relevant.

Contractors and clients should also review agreements regularly. If the project changes, the contract should be updated. A contract written for one type of work may not remain accurate if the role becomes broader, longer, or more integrated into the client’s team.

Independent contract reviews can also help. A specialist legal or tax adviser can identify risky wording and check whether the contract reflects the real relationship.

HMRC’s CEST tool can be used to help check employment status for tax and understand whether a change to a contract or working arrangement affects the result.

Contractors and clients should review agreements before signing. Do not rely on generic templates without checking whether they match the project.

Every contract should clearly define the services, deliverables, payment terms, responsibilities, and end date. The agreement should avoid employee-style wording and focus on a commercial service relationship.

Working practices should match the written contract. If the agreement says the contractor controls how the work is done, the client should not manage the contractor like an employee. If the contract includes substitution, the process should be realistic.

For outside IR35 engagements, contractors should also act like independent businesses. This includes keeping business records, holding insurance, using invoices, maintaining professional independence, and avoiding employee-style integration.

Clients should conduct regular compliance checks, especially when projects are extended or responsibilities change. Where necessary, both parties should seek professional legal or tax advice before accepting or offering contractor engagements.

The IR35 meaning refers to UK tax rules that decide whether a contractor working through an intermediary should be treated as employed or self-employed for tax purposes. If the contractor works like an employee, the engagement may fall inside IR35.

It means the contractor is treated as an employee for tax purposes for that specific engagement. PAYE tax and National Insurance may need to be deducted before the contractor is paid.

It means the contractor is working as a genuine independent business. The relationship is business-to-business, and the contractor is not treated like an employee for tax purposes.

An IR35 assessment usually reviews the written contract and the actual working practices. Key factors include substitution, control, mutuality of obligation, financial risk, integration into the client’s business, and whether the contractor operates independently.

No. A contract is important, but it cannot determine status on its own. Under IR35 rules, the actual working practices must align with the written terms. If the contract says one thing but the day-to-day relationship works differently, the actual relationship may carry more weight.

Contractor agreements are essential for managing IR35 risk. A clear, well-drafted contract can show that the contractor is operating as an independent business, not as a disguised employee.

However, compliance depends on more than wording. The contract must align with the actual working practices. Substitution, control, mutuality of obligation, financial risk, payment terms, and termination clauses should all reflect a genuine commercial relationship.

Contractors and clients should review agreements regularly, update contracts when projects change, and keep evidence of how the work is carried out.

Before accepting or offering a contractor engagement, seek a professional IR35 contract review. It can help you identify risks early, strengthen your agreement, and stay compliant with IR35 rules.